Summary

More than 85% of the world’s population lives outside Northern America and Europe. Rapidly growing, urbanising, and connecting populations are transforming the global geo-economic order across this vast and diverse ‘85 world’.

The old order of Western domination of technology, trade, economic might, and aspiration has given way to a world of multiplicity, as rising countries, cities, firms, and individuals – fuelled by unprecedented technological and physical connectivity and growing middle classes – are reconfiguring the global grid. The rise of the ‘non-Western’ world is here to stay, with far-reaching implications for how we produce, connect, consume, and live.

Part I - The Foundation

More than 85% of the world lives outside Northern America and Europe. This is not a demographic forecast, but our current reality and a trend that will continue to grow. Northern America and Europe will remain a demographic minority far into the future.

But it was not always this way. In 1900, Europe was home to a quarter of the world’s population. Today, it accounts for about 7%. Over the course of the 20th century, the ‘non-Western’ world’s population – Africa and Asia, in particular – grew more rapidly than Europe. Today, three out of fourpeople in the world live in Africa or Asia.

Population Growth in Europe vs the ‘Non-West’

Source: A. Maddison, 2008

For most of human history, the world has been poor, disease rife, and opportunity scarce. Extreme hardship has been the norm. But that has changed, with the most dramatic transformation taking place over the past three decades. As economist and development specialist Steven Radelet notes, 1bn people have been lifted from poverty since the early 1990s. Three decades ago, one in two people lived in extreme poverty. Today, it is one in six. But the story is broader than just one of poverty reduction, no matter how momentous and dramatic the numbers are. There is much still to be done.

We are living in an era of global geo-economic transformation comparable in importance to the Industrial Revolution. This transformation is centred on the rise of emerging markets and the growth of a new global middle class, as well as rapid urbanisation and increased physical and technological connectivity. These powerful economic drivers will continue to dramatically transform our world over the next several decades, lifting millions more out of poverty, reshaping global trade patterns, altering geopolitical alliances, creating new centres of innovation, and posing new and previously unimaginable challenges to societies and states.

Part II - The Age of Aspiration

Let us begin, appropriately, with China. It is hard to imagine a bigger geo-economic tectonic shift over the past 25 years than China’s rise. Its transformation, author Evan Osnos argues, moved at “one hundred times the scale and ten times the speed of the Industrial Revolution that created modern Britain”. From 2009 to 2011, China’s economy added up to 50% of all global growth. The country’s massive post-financial crisis fiscal stimulus also supported emerging market exporters that had fed off the massive China-demand engine.

Amid the country’s transformation, some 270m Chinese left rural areas to work in cities. Five years ago, China passed the 50% urbanisation mark, and it will never look back. The Chinese are the largest consumers of beer, movies, energy, and just about every major commodity. Chinese outbound tourism has become a global force in the travel industry, vaulting to number one in the world in terms of spending over the past few years. The Chinese middle class has become the holy grail for multinational companies, endlessly courted and studied. Apple CEO Tim Cook regularly highlights the importance of China’s middle class to his company’s fortunes.

To get a sense of the scale of the country’s building boom, consider this: China poured more cement and concrete between 2011 and 2013 than the US did through the entire 20th century. When China’s demand for commodities began to slow over the past three years, countries from Zambia to Brazil felt the sting, underscoring China’s importance to the fate of poor and middle-income commodity exporters.

China vs US Cement Use in Construction

Source: The Washington Post, 2015

In 1978, the average Chinese income was $200. Today, it exceeds $6,000. In 1981, 84% of Chinese lived in extreme poverty. Today, that figure is 6%. Such high-speed change is disorienting, no doubt, but as Osnos writes, “by almost every measure, the Chinese people have achieved longer, healthier, more educated lives”.

It is easy to get bogged down in the eye-popping statistics that tell the story of China’s rise, but Osnos rightly points out that the greatest change to come to China was “aspiration, a belief in the sheer possibility to remake a life”. And it is not just in China. Attitudes towards aspiration have changed across the emerging world. It is entirely common and unremarkable for the son of a farmer in Kenya or the daughter of a taxi driver in Egypt to aspire to a higher station in life – and it is equally unremarkable when he or she succeeds through entrepreneurial flourish, higher education, or migration, and climbs the economic and social mobility ladder.

The first quarter of the 21st century might be dubbed the age of aspiration. Just about everywhere in the emerge85 area of focus, people are seeking more – more education, more goods, more connectivity, more opportunity, more rights, more entertainment, more jobs, more of almost everything.

What’s more, global polling indicates that emerging markets and developing country populations tend to be more optimistic about the future than their advanced economy counterparts. When asked if their children will be better off than their parents, advanced economy respondents in the Pew Global Attitudes Survey responded with a resounding no: Only about a quarter thought their children would be better off. In the growth markets of the emerge85 area of focus, however, more than halfthought their children would be better off.

This optimism in the ‘85 world’ will have global implications. Over the centuries, the Chinese, Islamic, and Western civilisations have all contributed comparably to world civilisation. However, since the renaissance and ensuing cycle of reformation, enlightenment, and the Industrial Revolution, Europe and eventually – by virtue of kin and culture – the US sped ahead and created the modern world. The re-emergence of the 85 marks a potential rebalance of the global order. In this we do not necessarily see Western decline, but rather global invigoration.

What does a world with multiple active centres of economic and cultural production look like? This is essentially what we want to understand by studying the 85 world, and provide a platform for voices from these regions and for those who have devoted their lives to studying them. To help bring our plan to fruition, we have zeroed in on four parameters through which we intend to study and understand the re-emerging world. How will the 85 world:

- Produce (goods, services, and ideas);

- Connect with peers and with developed economies (import/export of the same);

- Consume (again, goods, services, and ideas); and

- Live (What will their cities look like? What entertainment options will they choose? How will they educate their children?).

We understand that the countries, regions, and cities in the 85% are distinct, with their own histories and narratives, counter-histories and counter-narratives, opportunities and challenges, cultures and counter-cultures. We do not intend to lump this diverse world into a convenient category, but we do believe that the world order dominated largely by the West for the past five centuries has – and is – shifting with the rise of the 85% in the last several decades. And this will have implications on how we produce, consume, connect, and live, not to mention aspire.

Part III - Produce

In a quarter of a century, Asia’s share of global manufacturing output has grown from a quarter to almost half. Behind this number is a wide array of economic actors – from large multinationals like the Tata Group and Huawei Technologies to the Shenzhen hardware hackers, the most famous of which is DJI. In addition to this, emerging multinationals are increasingly feeding the world – from Grupo Bimbo of Mexico, the world’s largest baked goods company, to JBS of Brazil, the world’s biggest meat and poultry producer, to Universal Robino, the Filipino food conglomerate supplying the ASEAN and Oceania region.

In the travel industry, who could have missed the dizzying rise of Dubai-based Emirates Airline, among the largest carriers in the world in terms of international passengers, or its emerging market competitors, Abu Dhabi-based Etihad Airways, Doha-based Qatar Airways, and Istanbul-based Turkish Airlines? These four airlines – all of which are at or near the top of best airline rankings – have impacted global commercial aviation in ways unimaginable two decades ago. They have also become global brand icons, their names adorning the jerseys of international football teams or attracting global actors and athletes.

The pharmaceutical industry represents an interesting – if less glamorous – case study. Emerging market pharmaceuticals have grown in revenue from $8bn to $80bn in just 10 years; this puts them at just under 10% of the global revenue of the industry. What is particularly worth noting is how India managed to negotiate a ‘compulsory licence’ that allows its local companies to produce generics in cases of major public health crises, all while still allowing for the likes of Sun ($4bn in annual sales) and Lupin ($2bn) to emerge as growing global players.

In fact, the two acts exist not in tension but, to some extent, in correlation. India’s key role in Africa in providing affordable HIV anti-retroviral medication in the 1990s has allowed it to benefit from the continent’s growth two decades later; in 2011, almost 20% of its pharmaceutical imports were from India. The African pharmaceuticals market, worth $21bn in 2013, is expected to grow to anywhere between $40bn and $65bn by 2020.

Throughout much of the 20th century, Western multinational companies were the dominant force in global commerce, with the late century exception of Japan and South Korea. People in Africa, Latin America, and Asia tended to be consumers of Western technology products and brands. Today, four of the top five best-selling smartphones globally are South Korean or Chinese brands.

One of the great untold stories of the past 15 years is the rise of the emerging market multinational willing and able to go head-to-head with Western multinationals operating in emerging markets, while reaching far beyond their home borders. According to a Boston Consulting Group, major emerging market multinationals have grown three times faster than their Western counterparts over the past decade. “The economies of some emerging markets may have paused … but not their strongest and most global companies,” BCG wrote in its 2016 study, ‘Global Leaders, Challengers, and Champions: The Engines of Emerging Markets’.

The multinational corporation is an invention of the Western world. In its early incarnations in the 16th-18th centuries, the multinational corporation was both a profit-driven enterprise and a tool of colonialism, often brutal, as in the case of the Dutch East India Company. We have come a long way from those days, but one thing remained constant until only a few decades ago: The near total domination of Western multinationals. That clear playing field for Western firms has now changed, and they are facing intense competition from emerging market multinationals capable of defending their own turf on competitive grounds, while also posing a challenge globally. This clearly illustrates the evolving fundamental shift in the global commercial order – one that we will track closely in the emerge85 lab.

Part IV - Connect

When we talk of connectivity, people instantly think of social media and, more broadly, the technological revolution. Lost amid this due recognition of software is the profound influence of ships and airplanes – hardware – on globalisation. Slow-moving, plodding ships, be they containers or tankers, are neither exciting nor telegenic. But they are vital to our way of life. About 90% of world trade takes place through shipping.

This industry is literally the arteries pumping blood throughout the global economy. It is the hard infrastructure of connectivity. A ship transported your phone to your local store; an airplane delivered crucial parts to build it.

An oft-quoted Chinese proverb says: “If you want to create wealth, build a road.” The maxim remains true, but to that, one might add a sea port and an airport as well. The more connected you are by air and sea as a city, a region, or a country, the better off you generally are. A glance at the UN Conference on Trade and Development Connectivity Liner Index, a measure of sea-based connectivity, demonstrates the value of ports: The most connected countries tend to be the most prosperous.

The same goes for thriving air hubs. Airports are no longer simply places to catch flights. The most dynamic ones have become economic ecosystems creating an ‘aerotropolis’ economy fed by trade, tourism, and broader ecosystems of support. Every day, 10m people board airplanes. Goods worth more than $18bn are sent by air each day, according to the International Air Transport Association (IATA).

The fastest-growing demand for air traffic comes from the Asia-Pacific region, and emerging markets more broadly. The rise of affordable, accessible air travel has shrunk our world. India is the fastest-growing aviation market in the world, according to IATA. Twenty-five years ago, a middle-class Indian could have spent his entire life without ever stepping onto a plane. Now, low-cost carriers like IndiGo – the market leader – have made air travel routine. Indians travel nine times more today than just two decades ago.

Now, imagine middle-class Indians landing somewhere in Africa. They might see a familiar name pop up on their mobile device when they connect: Bharti Airtel. The Indian mobile network operator is one of the largest players in Africa, and the third largest in the world. When it comes to mobile telephone networks, African, Asian, and Latin American companies predominate in their own markets, and play an increasingly significant role beyond.

Largest Emerging Market Mobile Networks

Source: BusinessTech, 2015

Six of the world’s top-ten largest mobile network providers hail from the 85 world – China Mobile, Bharti Airtel, China Unicom, America Movil (from Mexico), Axiata (from Malaysia), and MTN Group (from South Africa). Whenever a major new market opens to mobile network providers, the top three or four companies vying for the contract are often from the emerging world. Gone are the days when the West held all the magical tools of the technology of connectivity. Now, it is just as likely that a new market will be connected by a Malaysian or Indian or Qatari or Emirati or Turkish network provider.

Chinese President Xi Jinping has taken the aforementioned Chinese proverb – and a wealth of data to support connectivity – to a global level with the One Belt, One Road initiative, a series of infrastructure investment measures aimed at building up the connectivity of the Eurasian landmass and the seas surrounding Asia and Africa. This initiative represents one of the most ambitious policy measures to emanate from anywhere in the world over the past decade, though the idea is neither new nor revolutionary.

We are not impartial when it comes to infrastructure: We believe profoundly in the extraordinary catalysing power of infrastructure to grow economies, support innovation, and create jobs. Amid global talk of income inequality, we think infrastructure inequality deserves equal attention, and those countries in the 85 world that focus on the infrastructure of connectivity will see results far into the future.

It will come as no surprise that Singapore is the most connected city in the world. It sits atop most rankings that study connectivity, from the DHL Global Connectedness Index to the McKinsey Global Institute Connectivity Index. When Lee Kwan Yew became the prime minister of Singapore in June 1959, the country’s GDP per capita was $550. Today, it is $55,000. Singapore owes much of this stunning rise to its connectivity.

Clearly, Lee was a statesman ahead of his time, and understood the power of trade. It was only three years before he became Singapore’s first prime minister that the shipping container was invented, an innovation that revolutionised our world. The author Marc Levinson recalls the “beginning of a revolution” on April 26, 1956 when “a crane lifted 58 aluminium truck bodies aboard an ageing tanker ship moored in Newark, New Jersey”.1 That revolution produced container shipping, which laid the groundwork for the rise of Singapore.

The Port of Singapore is an economic colossus. It is the world’s largest transshipment centre and the second-busiest container terminal port by total tonnage after Shanghai. Remarkably, it also ships about half of the world’s globally traded crude oil. Today, Singapore sits at the centre of the fastest-growing trading continent in the world. Asia has served as the engine of global trade growth for the past decade. In 1995, according to the World Trade Organisation (WTO), developing countries imported $487bn worth of goods. Today, that number is nearly 10 times higher, exceeding $4trn.

Much of that rise is a result of the great Asian demand engine, powered by China, but increasingly dispersed to other fast-growing states on the continent, notably the Philippines, India, Malaysia, Vietnam, Thailand, and Indonesia. As the Asian Development Bank notes, despite economic headwinds, Asia will continue to provide 60% of global growth in 2016 and 2017.

The Asian middle-class consumer has emerged as one of the most powerful economic drivers of the future. By 2030, according to some estimates, Asia will host nearly two-thirds of the global middle class, and they will account for 40% of global consumption. Besides, Asia is not just driving demand growth, but also export growth. According to the WTO, Asia “did more than any other region to lift merchandise export volume growth between 2011 and 2014”.

China’s economic strength, the export-driven economies of South Korea and Japan, rising Malaysia and Indonesia – all owe a debt to the great container ports of Asia like Hong Kong, Singapore, Shanghai, Shenzen, Busan, and Tokyo. There is a multiplier effect in hub cities and trading nations that is sometimes difficult to measure, and Singapore and Hong Kong have amplified and multiplied Asia’s growth over the past three decades.

The UAE is another country that can be seen as an amplifier and multiplier of others’ growth. Dubai’s Jebel Ali port has emerged as the ninth-busiest container terminal port in the world, and a global transshipment centre that connects Africa to Asia, Europe to the Middle East, and beyond.

The UAE’s principal airports – Dubai and Abu Dhabi – handle more international air passengers than Frankfurt International and Seoul’s Incheon combined. Dubai International Airport surpassed London’s Heathrow as the busiest in the world in terms of international passengers in 2014, and is a vital connector for South Asia and sub-Saharan Africa to the rest of the world.

The growing Dubai-Abu Dhabi economic corridor is creating a powerful new urban conglomeration, leveraging the oil wealth and policy energy of Abu Dhabi with the trading hub and innovative energy of Dubai. Today, the UAE’s GDP is 140 times larger than it was in 1973. Yes, the UAE benefitted from oil wealth, but others have oil, too. That level of GDP growth is only possible with an outward-looking focus on trade and the building of an infrastructure of connectivity.

Part V - Consume

The most-visited lifestyle destination in the world is a mall. The Dubai Mall, to be precise. The retail colossus attracts more than 80m visitors a year, many from the emerging markets’ middle classes who are driving retail growth across the world. Ranking right up there is a grittier, lower-end mall across town, Dragon Mart, the largest Chinese wholesale retailer outside of China.

It is fitting, in a sense, that a mall would take top prize as the most-visited lifestyle destination in the world. After all, we are a world of consumers, and no consumer group holds more promise than the urban, middle class, emerging market consumer.

Global consulting firm EY suggests that we are living through history’s third great, middle-class expansion. The first encompassed Western Europe and the US during the Industrial Revolution, the second included Western Europe and the US again, with the addition of Japan in the post World War II period. The third expansion is being driven by emerging markets.

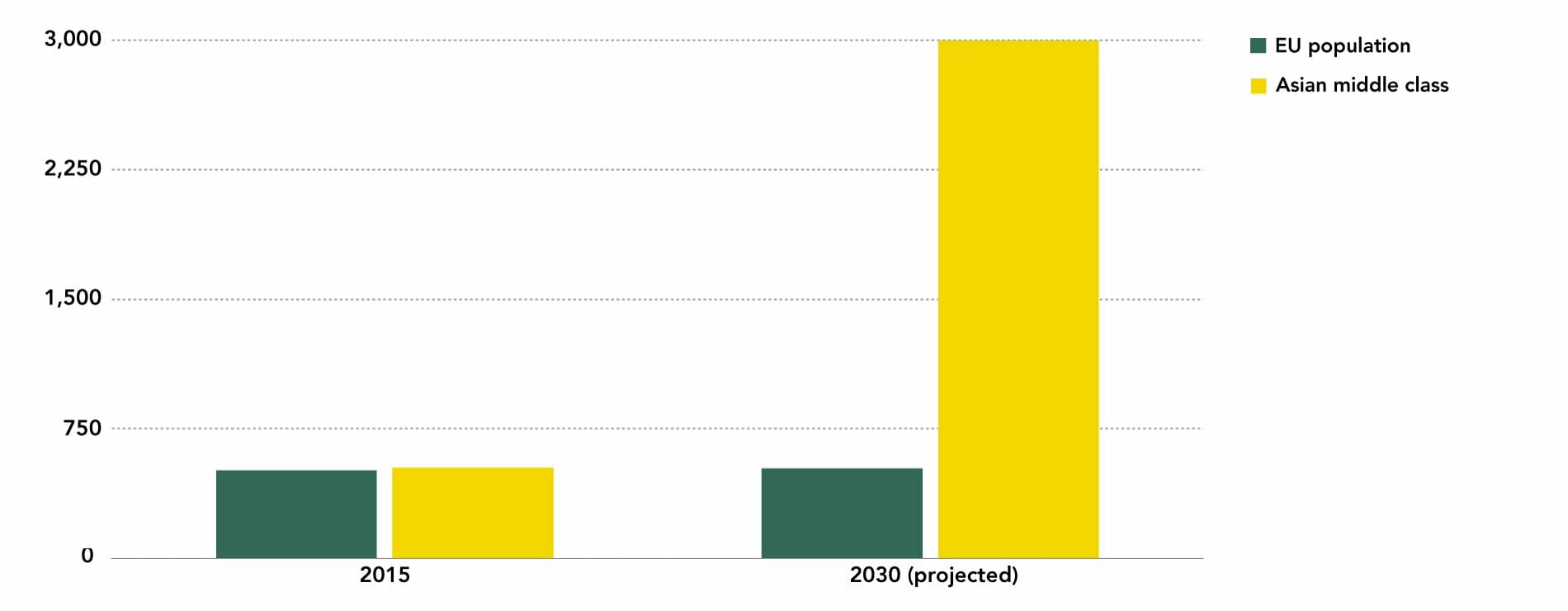

As EY notes, “In Asia alone, 525m people can already count themselves middle class – more than the EU’s total population. Over the next two decades, the middle class is expected to expand by another 3bn, coming almost exclusively from the emerging world.” This means, as EY notes, that “companies used to serving the middle-income brackets of the old Western democracies need to decide how to supply the new bourgeois of Africa, Asia, and beyond”.

Projected Growth of the Asian Middle Class vs EU Population

Sources: EY, 2013; Eurostat, 2016

We view the race for the global, emerging middle-class consumer as the great commercial prize of the 21st century. The race is already on – and has been for about two decades, actually. Nestle, Unilever, Johnson & Johnson, Proctor & Gamble, Starbucks, and others are all actively on the chase. Many of the biggest global multinationals such as Unilever and Nestle earn more from emerging markets than they do from the West, and some of the rising multinational stars that hail from emerging markets are also expanding their bottom line by serving their home markets and beyond.

Thus, while the growing middle classes in Asia, Africa, and elsewhere are strolling air-conditioned malls, they are carrying in their bags not just a new pair of shoes or a new smartphone case, but the fate of the global economy, too.

Part VI - Live

“Sometimes the wrong train can take you to the right destination.”

From the critically acclaimed 2013 Indian movie, The Lunchbox, set in Mumbai.

Cities are human laboratories for our greatest achievements as well as our basest instincts. A city like Mumbai – chaotic, dynamic, tragic, extraordinary – can both inspire us and remind us of the cruel fate of man.

Over the next 14 years, there will be another billion urban dwellers globally. By the year 2050, two out of three people in the world will live in cities. Most of this growth will come from the emerge85 world. The fate of nations is increasingly tied to the fate of their most dynamic cities. Seoul accounts for about half of South Korea’s $1.3trn GDP, and Jakarta accounts for more than a quarter of Indonesia’s economy. All across the world, urban economies are driving national economies.

Of the 291 financial institutions based in Seoul, 93 are headquartered in Yeouido. September 26, 2008. InSapphoWeTrust/Flickr CC BY-SA 2.0

Today, more than half of the world’s population lives in cities. In 1900, only 12 cities had more than a million people. Today, more than 400 cities do, particularly in the 85 world. The largest mega-cities in the world are all in Asia, except for one: New York. Tokyo retains its title for the 60th year as the largest city in the world.

Cities will define our future. They are not only economic engines, but also sources of innovation that empower us with new technologies, creativity, pop culture, and laboratories for new products and new businesses. The urbanist and demographer Joel Kotkin noted that “cities, in a word, are about people, and to survive as genuine, real places, that are distinct and unique, this is what they need to be about”. We are intensely curious about cities, middle classes, and connectivity because, ultimately, we are curious about people.

Many of the cities in the 85 world are new, their infrastructure built more recently, unencumbered by legacy infrastructure. Indeed, a prerequisite for success for emerge85 cities tends to be getting the hard infrastructure right: The roads, ports (sea and air), broadband, and the like. Between 1992 and 2011, China, Japan, India, and the Middle East, and Africa respectively spent 8.5%, 5%, 4.7% and 3.6% of their national GDP on infrastructure. Meanwhile, the US and EU spent 2.6%. The only 85 region lagging behind them was Latin America, at 1.8%.

Combined with the very different political, economic, and social contexts in which these cities are built, the ‘newer’ cities can be constructed in vastly different ways, from scale to method to purpose. Their need to build bigger cities faster, cheaper, and, in many cases, in virgin or demolished plots means they are highly unlikely to build cities in the same way the West has. What will those cities look like? How will their occupants co-opt them and be co-opted by them? What does that kind of user and designer tension look like in an emerging market in a super-connected era?

Part VII - Curiosity

And where is ‘there’? The growth economies of the 85 world will not re-emerge independently; the world is too connected. The 85% will impact the 15% and be impacted by the present and future of the 15% just like its past – while impacting its neighbours and the region. It will make for a complex theatre of innovative co-operation and tense friction. Is there room for everyone at this specific moment in the global order? Will China build a parallel one? Will Brazil re-emerge from its current troubles and finally ‘arrive’? Will young Africa really be a quarter of the world’s population, and probably an even higher proportion of its consumers, by 2050? Is the Abu Dhabi-Dubai nexus a 21st-century Singapore lifting the region – from Africa to West Asia? These are some of the questions we intend to spend time comprehensively asking, iteratively refining, and hopefully answering.

And, there is no kool-aid to drink. Even if the 85 world goes by the way of Japan and deflates for decades on end, it will still matter a great deal. The 85% is here to stay. Something new is happening there with agency and aspiration. Such happenings were last seen in the West half a millennium ago. And there is not battlestar exotica, it is where I’m from (Mishaal) and where I lived and first worked (Afshin). It is also where the vast majority of our human world lives today – and tomorrow.